How hedge funds and brokers have manipulated the market.

By Lucy Komisar

The American Prospect, June 22, 2021

JOHN MINCHILLO/AP PHOTO

In the aftermath of the GameStop run-up in January, retail investors found telltale signs of a common yet egregious trading fraud by major brokers and hedge funds.

I have written previously for the Prospect about the frenzy over GameStop (GME), the video game and electronics company. By now, you know the story. Millions of retail investors made the stock soar by over 1,000 percent in January 2021. This brought disaster upon a handful of hedge funds that had bet on GameStop’s stock to drop. According to Markets Insider, one analyst estimated losses in February of roughly $19 billion. The hedge fund Melvin Capital reportedly closed out its position after taking a drubbing of 51 percent. Another fund, Maplelane, lost 40 percent.

The rally eventually subsided, and the stock fell, though it remains well above its original price. But as retail investors looked into the details in the aftermath, they found telltale signs of a common yet egregious trading fraud by major brokers and hedge funds, which evaded what could have been far bigger losses. What happened around GameStop can be explained only by massive counterfeiting of shares.

The Securities and Exchange Commission (SEC), which along with other regulators could confirm whether the patterns seen in GameStop trading constitute fraud, has known about and largely ignored practices like this for years. The financial media also ignores this systemic corruption.

Here’s how it works.

Naked Short Selling and Fails to Deliver

The SEC allows traders to short a stock, which means to sell it even if they don’t own it, hoping to buy it back later at a lower price and bank the difference. Short sellers borrow the stock, usually from a broker, who either has it in their inventory, borrows it from another broker, or vows to “locate” the stock when the time comes and cover the short.

That promise is often fake. A broker handling several sellers will borrow synthetic or manufactured shares, or “locate” the same stocks for multiple shorts. Traders and brokers have been mildly sanctioned for this scam.

Sellers are supposed to send shares to buyers within two days. If they don’t convey the stock, there is a failure to deliver (FTD). This is also known as naked short selling. Traders that have outstanding FTDs are required to transfer the shares within a given time and are restricted from selling short until then. This rule is massively ignored or finessed, and the penalties are minor.

The major GME short sellers had to cover their shorts at a time when the funds had shorted much more stock than existed and when owners with real shares weren’t selling, even at higher prices. They were threatened with a short squeeze, with the price going so high that they cannot cover it with existing assets, and they get a margin call, a demand that additional money gets dropped into their brokerage account.

The short squeeze ended under peculiar circumstances. A January 28 spike in GME led Robinhood, the online broker that handled orders for many retail traders, to cut the buy option for the stock from its app. Robinhood CEO Vlad Tenev told the House Financial Services Committee in February that he had discussed the trade restrictions with the Depository Trust and Clearing Corporation (DTCC), which clears public trades, after it made a $3 billion margin call.

However, DTCC CEO Michael Bodson told the committee in May that “the decision to restrict trading really was internal to Robinhood, we did not have discussions about that.” He noted that with Robinhood, “the system worked.” It stopped the buys while the big traders continued to sell. GME that day hit $483, but then the price plummeted, and the short squeeze was over.

Why would Robinhood shut down GME trading? It did not lose money on trades, because it did not have its own investments. The answer may be hidden in the murky relationships involving market makers and hedge funds.

Citadel Securities, a market maker, handled Robinhood’s orders on a “pay for order flow” basis (it paid for orders routed to it), which equaled 40 percent of Robinhood’s revenue. Citadel Securities is a division of a company founded by billionaire Ken Griffin. Another division, the Citadel hedge fund, helped provide short seller Melvin Capital with nearly $3 billion in funds during the GME short squeeze. Citadel Securities would have the clout to persuade Robinhood to shut down trading, and the motive, given its other division’s investment in Melvin. (UPDATE: Robinhood COO James Swartwout stated in sworn court testimony in February for a case in California that “no third party, including either Citadel or Citadel Securities, requested that Robinhood apply restrictions on stock or options trading or played any role” in the decision to limit trading.)

Citadel Securities also has a knack for running afoul of the trading laws. It has been fined 58 times in the last few years for violating trading regulations, many about naked short selling. In February 2021, the same time frame as the GME trades, Citadel Securities was fined $10,000 for failing to close out a failure to deliver of shares it had sold short.

Meet the Investigators

There are conflicting arguments about whether GME was a battle of long and short hedge funds, whether retail investors through Robinhood and other trading apps played a significant role, or maybe both.

Robert Shapiro, chairman of the economic advisory firm Sonecon and undersecretary of commerce for economic affairs under Bill Clinton, believes the war between hedge funds theory, with a healthy dose of “pump and dump” market manipulation and naked short selling. Shapiro has testified before the SEC and criticized it for failing to take effective measures against naked shorting.

Writing in Washington Monthly, Shapiro explained, “The nearly five-fold jump in GameStop’s average trading volume from July to December signaled that large institutional investors were buying [and selling] the stock … The wild swings in those share prices reflect hundreds of millions of shares being traded each day, mostly in big blocks and presumably from one hedge fund to another.” He estimated that some 20 million or more of the GameStop shorts were never borrowed and never delivered to their buyers.

Additional documentation of the GameStop manipulation comes from a handful of people on the WallStreetBets spinoff site Superstonk, who have painstakingly analyzed filings to the SEC and FINRA (the brokers’ “self-regulator”), stock reports from Bloomberg, and other public sources. (“Stonk” is their hokey way of saying stock.) Much of the data reported here is taken from their posts, which are all public and verifiable.

It’s important to note that only the SEC and the DTCC can get the trading documents that would show proof of any fraudulent scheme. But the Superstonk users, through publicly available data, detected patterns that make a strong case at least to investigate the matter.

For example, u/broccaaa, a Superstonk user, looked through SEC filings for funds with large GME positions. Big losers like Melvin and Maplelane had no shares in GME, and large puts, which are options to sell. According to u/broccaaa, this is a common characteristic in stocks with large unsettled trades, where the shares have not been transferred. He described it as “supportive evidence for naked short trades … around the end of December and early January short interest and fails to deliver were through the roof.”

The float is the number of shares a company has issued that are available for investors to trade. All the shares are held in the DTC (Depository Trust Company), the “vault” of the DTCC, and “owners” have only digital entitlements. In the run-up to the short squeeze, Bloomberg Terminal data routinely showed well over 100 percent of GME float held by institutions, not including retail investors. (This ramped down massively after the short squeeze.)

Some of the extra shares result from the fact that, during the time between a short sale and settlement, both parties have legitimate digital entitlements. And due to the nature of SEC filings, there could be double counting. But the evidence shows that many of those shares never settled. The issue is fails to deliver.

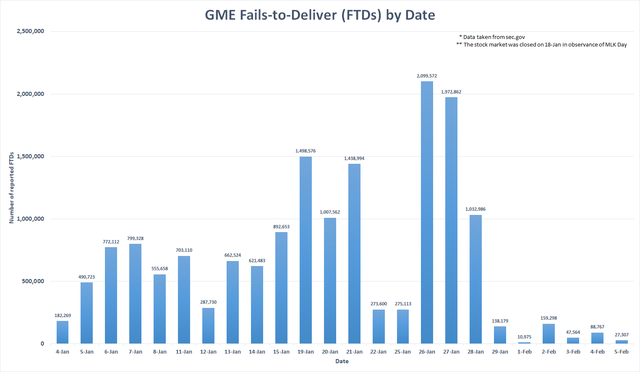

Under SEC rules, shares of companies that fail to deliver in the previous five trading days are put on a “threshold list.” GameStop’s first date on this list was September 22, 2020.

Shares failed in massive numbers in the following months, leading to GameStop being put on the threshold list for 39 days between December 8 and February 3, with hundreds of millions of shares failing to deliver.Expand

CHART BY U/NAYBOYER2. DATA VIA BLOOMBERG.

How could GME be on the list for so long? Regulators have the authority to find out which brokers failed to deliver, facilitating naked shorts. But the DTCC has historically beaten back attempts to reveal naked short selling culprits, or even to tag “borrowed” shares (called the hard borrow) so they can’t be “located” more than once. I’ve written previously about how DTCC pulled back on backing a centralized database that would prevent the same shares from being used for multiple short sales.

“There is no lawful way for a stock to be on the threshold list for months,” said John Welborn, who teaches economics at Dartmouth. “The only explanation is regulatory apathy, or worse.” Because compliant regulators choose not to track shorts, traders can engage in mischief.

But how can we know that counterfeit shares were created for GME?

The Big Scam

In 2007, online retailer Overstock sued the major prime brokers for naked shorting its stock and creating counterfeit shares that flooded the market, causing its share price to drop from $70 to $20. It presented evidence that Goldman Sachs created fake inventory for stock lending.

Here’s how an insider described it in a 2011 Overstock court deposition: “A firm or a market maker would synthetically create a short position by doing option trades in it, buying the stock, selling a call or buying a put or this, that and the other. And by buying the stock, they could create a borrow off an option trade.”

In the conversion trade, an options market maker is on one side, and a prime broker on the other. It isn’t real market making, which is to be in the middle so all traders can buy or sell shares, or in this case, options. “The goal of the trade is to get the prime broker loanable inventory of stock,” Welborn said.

How do you get there? You get there by this conversion trick. First, the options market maker sells the prime broker a naked short that never settles from the market maker. This is “the most important leg of the trade,” Welborn explained. The market maker also sells a put option (an option to buy the stock in the future) to the broker. This gives the market maker a neutral position, but the broker can maintain a “long” position, as if they owned the stock.

The broker can now lend that stock out to multiple clients. In this way, the prime broker and the market maker are creating fake lendable shares out of thin air. The end result is organized counterfeiting of shares in the market.

Regulators aren’t providing enough transparency to ferret it out. As Welborn said, “Regulators tell us there are fails but don’t tell us who did the fails. Liquor stores are being robbed, but they don’t tell us who robbed the stores.”

There is voluminous evidence from the Overstock case of Goldman Sachs engaging in this practice, including an email from a broker conceding that such conversion trades “create inventory to allow customers to short.” When Overstock got the incriminating evidence, after Goldman’s lawyer posted it by mistake on PACER, the federal court online filing system, Goldman settled with Overstock in 2015 for $20 million.

Massive Shorts and Short Interest

An obvious sign of market manipulation is massive short interest, the number of shares that have been sold short but not yet covered. These could be legally borrowed shares that were first located. However, GameStop did have more than 100 percent short interest, including 140 percent in January, which means more shares were reported as being short sold than all the shares that should be available to trade.

u/rainforest11 of Superstonk explained that FINRA reported short interest at 226 percent of total float at the height of the GME frenzy in January. This means that more than twice as many shares as exist in reality had been sold short at one point. As late as January 28, it was reported by S3, a market data company, to be 122 percent.

Counterfeit shares were likely used as “loans” to cover the naked short attacks that knocked down the share price. With short interest well above 100 percent of the float, there were not enough real shares to borrow. That is why there were fails to deliver to the buyers.

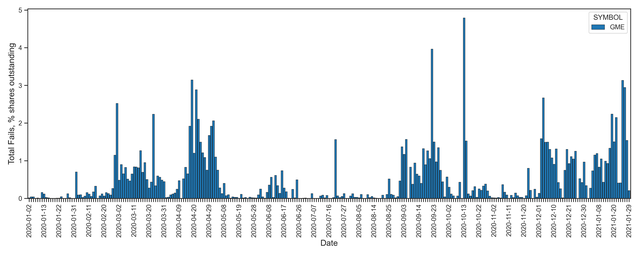

The chart below shows the percentage of GameStop shares that failed to deliver between the beginning of January 2020 and the end of January 2021. The FTDs, between 1 and 5 percent of total shares, may seem like small numbers, but as the website Where Are the Shares asks, “Would it be okay if 1 percent, 2 percent, 4 percent of your bank deposits failed to show up?”Expand

CHART BY U/BROCCAAA

The short squeeze was nearly a disaster for the hedge funds. u/rainforest11 explained, “Assuming the [share price] rocketed to $1,000 or beyond … hedge funds would likely go bankrupt as financially speaking there would be no way they would be able to cover all their shorts, and presumably entities that lent the short side hedge fund the shares to short would be holding the bag.”

But although GME’s momentum was at an apex on January 28, with the stock jumping to $513 a share in pre-trading, Robinhood suddenly shut off the ability to buy GME. Several other brokers followed. Immediately after this block on buys, FTDs and short interest dropped massively. The price also nosedived, which is what the naked shorters wanted.

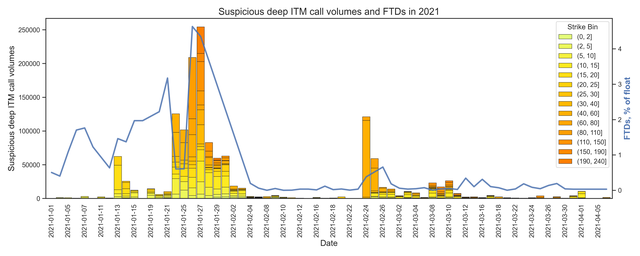

u/broccaaa wanted to prove the manipulation, how naked short sellers can acquire shares and close the FTDs. He designed an algorithm to detect a type of option known as a “deep in the money (ITM) call,” which allows buyers to purchase shares significantly below the market price.

“As FTDs were spiking and the situation became more and more unsustainable for the shorts towards the end of January, illegal Deep ITM options purchasing was used to naked short and cover FTDs,” he said. The chart below, compiled from historical options data, shows that on January 27, 25 million shares were acquired in this fashion. Overall, this technique conjured up to 150 million naked short shares. The blue line on the chart tracks fails to deliver as a percentage of float. These nearly disappear after January 27.Expand

CHART BY U/BROCCAAA. DATA FROM MARKET CHAMELEON.

Other Scam Tactics

A married put is a legal options trading strategy where an investor in a stock buys a put (an option to sell) on the same stock, to protect against depreciation in the stock’s price. Crooked hedge funds will simultaneously purchase puts from a market maker and buy shares of an equal number. In this way, the hedge fund obtains “phantom” shares from the market maker, which can be used to cover old positions or to sell on the market to suppress the price.

The SEC in 2003 expressed concern that “[s]ome strategies may involve the manipulative sale of securities underlying a married put as part of a scheme to drive the market price down and later profit by purchasing the securities at a depressed price.” It called them “sham transactions” which might violate the SEC’s anti-fraud and anti-manipulation provisions.

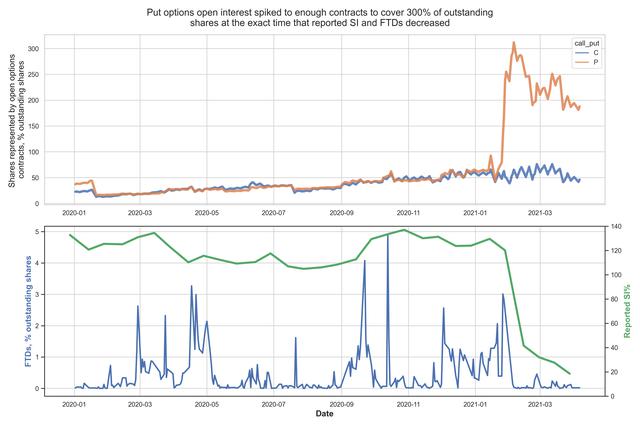

This appears to have been at work in GME, according to the Superstonk users. A 13F form must be filed quarterly with the SEC by institutional investors with at least $100 million in shares. These filings for the biggest known GME short sellers showed a tremendous amount of puts. New put option contracts after the end of January represented more than 300 percent of shares outstanding, more than 200 million shares. “Melvin Capital, which lost 50 percent of its value, had 6 million shares in puts,” said u/broccaaa. This massive spike suggests that short positions have been hidden using “phantom shares” and “strategic fail-to-delivers.”Expand

CHART BY U/BROCCAAA

As u/broccaaa says, “This spike coincides perfectly with the drop in reported short interest and FTDs.” He sees it as “the most damning evidence of massive manipulation.”

The options scam can also reset the clock on fails to deliver. Remember that short sellers have two days to locate a stock to prevent an FTD; market makers and other authorized participants may have up to six days. The SEC explained a trading strategy known as “buy-write” in a 2013 paper. As Investopedia explains, “A buy-write is an options trading strategy where an investor buys a security, usually a stock, with options available on it and simultaneously writes (sells) a call option on that security.” This recycling of positions shows as a new transaction, so the short sale timer is reset. And the trader may never deliver the shares, because he can roll over the trades and do the deal over and over.

GME short positions could also be hidden in exchange-traded funds (ETFs), a basket of stocks similar to a mutual fund. u/broccaaa’s research shows that fails to deliver migrated from GME to ETFs in January 2021. The total value of reported short interest (GME + ETFs) remained as high as ever, at over $27 billion owed.

An SEC Loophole Allows FTDs to Continue

In spite of knowing how fails to deliver represent sham trades, the SEC has facilitated big brokers and hedge funds continuing the con, using a system where FTDs go to die: dark pools, which began in the 1980s and now handle more than 40 percent of trades.

Dark pools are opaque private exchanges run by the major banks and prime dealers, and they are inaccessible to other investors. They were created to settle large trades by hedge funds and institutional investors without moving the markets.

As the SEC said in 2015: “The close-out requirement applies only to fail to deliver positions in an equity security at a registered clearing agency.” So unsettled trades could migrate to dark pools, out of the sunlight where investors can’t see what is going on, and never be closed out. It is called “ex-clearing,” off exchange. It is naked shorters’ “get out of jail free” card.

The SEC has described transactions outside the clearing agencies as “rare.” Forty percent of all transactions is nowhere near rare!

Market makers like Citadel Securities facilitate dark pool transactions, without the market being aware of the transaction price. That prevents the transaction from impacting the share price on the public exchanges. In this fashion, GameStop manipulators could buy in a dark pool and sell on an open exchange, making money on the transaction.

Citadel’s market-making division has a history of being caught manipulating markets. The New York Stock Exchange (NYSE) said Citadel Securities “erroneously sold short, on a proprietary basis, 2.75 million shares of an entity causing the share price of the entity to fall by 77 percent during an eleven-minute period. In another instance, according to the NYSE, Citadel’s trading resulted in “an immediate increase in the price of the security of 132 percent.”

A Citadel spokesperson responds: “Citadel and Citadel Securities have always operated with the highest standards of integrity. Neither firm has ever been accused of or fined for market manipulation, and the claim that there is a ‘history of being caught manipulating markets’ is completely false.”

And NYSE president Stacey Cunningham said last week that so-called “meme stocks” like GME are prime targets for this manipulation. “The vast majority of order flow can trade off of exchanges, which is problematic,” Cunningham said at a CNBC conference. “That price formation is not really reflective of what supply and demand is.”

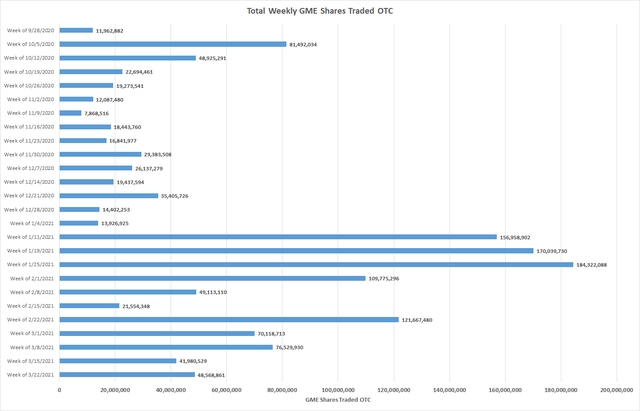

u/broccaaa compared his historical options data, which showed patterns consistent with naked shorting tricks, with dark pool trading volumes by known short funds. FINRA data since November 2020 showed GME activity ramped up massively at the start of January. Data shows that 25 percent of the GME float is traded OTC (over the counter in a dark pool), compared to less than 1 percent for major stocks.Expand

CHART BY U/NAYBOYER2. DATA FROM FINRA.

Note the spike in GME dark pool trades at the end of January 2021, especially the week of January 25, when the short squeeze was shut down. The big investors who trade in dark pools increased their volume till just that week when the price dropped.

u/broccaaa said, “When prices really started to move from January 25-29, more than 100 million shares were created with Deep ITM call and married-put naked shorting and used to hammer down price and hide short interest.”

He postulated that a coordinated blocking of buy orders at key retail brokers helped the shorters knock down the price. Over 525 million shares traded in January, and over 300 million in February. To put that in perspective, the GME float is somewhere between 26.7 and 50 million. Much of the trading took place in dark pools where the hedge funds operate. Since then, the average trade size has decreased to less than 50 shares per trade, per FINRA.

Data retrieved by Superstonk users all points to massive dark pool trades of GME. In February, 2021 volume traded as a percentage of float was 234 times higher than what it was for blue-chip Dow Jones stocks. Dating back to September 2020, between 40 and 69 percent of weekly volume was being routed off exchange.

Who was trading? u/nayboyer2 explains: “Based on their SEC 13F filing, Citadel owned only 217,132 shares. Prior to January, its previous high for number of trades was 75,652. But in January, Citadel traded over 252 million GME shares in the OTC market. In January, it traded over 1,161 GME shares for every one share that it owned.” Citadel is a high-frequency trading market maker, which means it can access more shares than it owns. But this level of trading activity is notable.

The Size of the Trades Raises Questions

Toward the end of January, as prices spiked during the run-up to a squeeze, the total number of trades more than quadrupled, but the average trade size dropped. There was a curious phenomenon of hundreds of thousands of micro transactions, trades of just a few shares, even one share each. But dark pools are set up to handle massive trades that must be hidden because they might otherwise “move the market.” The key players were known short funds.

Data from Superstonk shows that Citadel made over 1.98 million OTC trades during the week of January 25 and over 1.496 million OTC trades during the week of February 1. For nine weeks, 77.7 percent of trades were for under 60 shares.

In February, when Robinhood resumed allowing retail investors to buy stock, it limited buys to one share per trade. Furthermore, FINRA data shows that Robinhood Securities showed up on OTC trading for the first time during the week of February 8.

Why did Robinhood take the trades of its clients and move them through a dark pool instead of through Citadel? And why one share per trade?

Some subsequent correlations are worth noting. GME’s share price suddenly dropped from $348 to $172 in minutes on March 10. During that week, Robinhood was the top OTC trader and had one share per trade. The following week, Robinhood also traded heavily OTC, with 297,276 shares traded 297,194 times. This also correlates with large price drops in GME.

As u/nayboyer2 said in April, “Since Robinhood entered the OTC marketplace on the week of 2/8/2021, they have made 2.357 million trades with 2.362 million shares, for an average of exactly 1 share/trade.”

Trading single shares through dark pools, designed for massive trades, is using sophisticated high-frequency trading to manipulate the market. The SEC has expressed concern about the use of dark pools for small trades. Superstonk user u/nayboyer2 asked, “What in the actual hell is going on behind the scenes to allow this kind of OTC trading to continue, undisturbed, for almost 3 months?”

What are the SEC, FINRA, and the DTCC doing in the face of such apparent market manipulation? The SEC is reviewing payment for order flow, as well as whether off-exchange trading distorts stock prices. But at a May 6 House Financial Services Committee hearing about GameStop, Gary Gensler (SEC), Robert W. Cook (FINRA), and Michael C. Bodson (DTCC) and their congressional questioners never mentioned naked short selling, fails to deliver, or other documented indicators of market corruption. These regulators are the only ones who can truly unravel this mystery.

This story has been updated with Citadel’s response.

It seems they are perfecting this kind of thing now. The data for $CLOV from the end of June shows nearly 6 millions shares were failed to deliver.

6 MILLION SHARES! Most stocks might hover around the 100k mark for FTD on the high side. 6 million is just crazy town.

I normally don’t put on the tin foil hat but this sure smells awfully fishy.